The Bottom Line

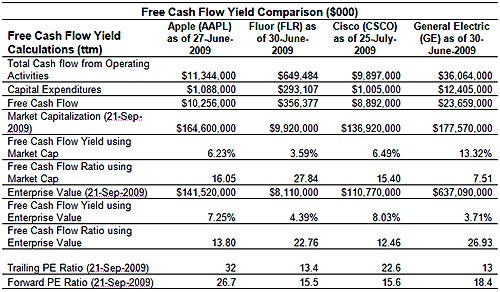

Free cash flow yield offers investors a better measure of a company's fundamental performance than the widely used P/E ratio. Investors who wish to employ the best fundamental indicator should add free cash flow yield to their repertoire of financial measures.

Like any indicator, you should not depend on just one measure. However, it is appropriate to employ measures that give you a fair picture of the fundamental performance of the company you are considering. Free cash flow yield is one such measure.

In an era when corporate earnings can easily be obfuscated by the rotating door of GAAP methodologies4, it is refreshing to be able to rely on a valuation metric that is difficult to manipulate or misrepresent. Free cash flow is one such measure, and it is attractive for its transparency.

Free cash flow is the cash that is left over after a company has made the appropriate allocations to maintain or grow its asset base (working capital and capital expenditures). Essentially, this pool of “free cash” allows a company to pursue shareholder-friendly activities, such as paying dividends, making acquisitions, and paying down outstanding debt.

The chart below was adapted from research conducted by Empirical Research Partners – it depicts relative returns for U.S. large cap stocks sorted by dividend growth, share repurchases, and price/free cash flow over the 35-year period from 1970-2005.

You will notice the following:

* Strategies focused only on dividend growth have only modestly outperformed the S&P 500 Index.

* Companies that pay no dividends at all have the worst return records.

* Strategies focused on price/free cash flow were the most effective at outperforming the S&P 500 Index.

Even in today’s severely compromised market environment, companies are fiercely protective of their free cash flow. Despite the downturn, free cash flow has held up remarkably well due to a couple of factors: a low capital expenditure base and aggressive management of working capital.

ต่อ

ด้วย

Cash Flow vs

"Owner earning"

เรื่อง cash flow มีพูดถึง ใน Buffet way ของ Hagstrom

แต่ ถ้า buffet เขียนเอง "Owner earning" กับ

Purchase-Price Accounting Adjustments and the "Cash Flow" Fallacy

อยู่ใน ปี 1986

เปรียบเทียบ สอง บ.

between O and N http://www.berkshirehathaway.com/letters/1986.html

What does all this mean for owners? Did the shareholders of Berkshire buy a business that earned $40.2 million in 1986 or did they buy one earning $28.6 million? Were those $11.6 million of new charges a real economic cost to us? Should investors pay more for the stock of Company O than of Company N? And, if a business is worth some given multiple of earnings, was Scott Fetzer worth considerably more the day before we bought it than it was worth the following day?

..

"Cash Flow", true, may serve as a shorthand of some utility in descriptions of certain real estate businesses or other enterprises that make huge initial outlays and only tiny outlays thereafter. A company whose only holding is a bridge or an extremely long-lived gas field would be an example.

But "cash flow" is meaningless in such businesses as manufacturing, retailing, extractive companies, and utilities because, for them, ( c) is always significant. To be sure, businesses of this kind may in a given year be able to defer capital spending. But over a five- or ten-year period, they must make the investment - or the business decays.

Why, then, are "cash flow" numbers so popular today? In answer, we confess our cynicism: we believe these numbers are frequently used by marketers of businesses and securities in attempts to justify the unjustifiable (and thereby to sell what should be the unsalable). When (a) - that is, GAAP earnings - looks by itself inadequate to service debt of a junk bond or justify a foolish stock price, how convenient it becomes for salesmen to focus on (a) + (b). But you shouldn't add (b) without subtracting ( c) : though dentists correctly claim that if you ignore your teeth they'll go away, the same is not true for ( c) . The company or investor believing that the debt-servicing ability or the equity valuation of an enterprise can be measured by totaling (a) and (b) while ignoring ( c) is headed for certain trouble.

"These represent reported earnings plus depreciation, depletion, amortization, and certain other non-cash charges...less the average annual amount of capitalized expenditures for plant and equipment, etc. that the business requires to fully maintain its long-term competitive position and its unit volume....Our owner-earnings equation does not yield the deceptively precise figures provided by GAAP, since capital expenditures must be a guess - and one sometimes very difficult to make. Despite this problem, we consider the owner earnings figure, not the GAAP figure, to be the relevant item for valuation purposes."

What Warren Buffett defined is identical to free cash flow.

FCF จาก Investopedia:

FCF is calculated as:

EBIT(1-Tax Rate) + Depreciation & Amortization - Change in Net Working Capital - Capital Expenditure

It can also be calculated by taking operating cash flow and subtracting capital expenditures.

ซึ่ง ดู เหมือน

จะเอา

Net Income ตั้ง

หักด้วย

Depreciation Depletion & Amortization

และหักด้วย

Capital Expend

="Owner Earning"

Slide:39 Steps in valuation

Calculate Owner Earnings over the past years.

Calculate the growth rate of Owner Earnings.

Estimate the future growth rate, and calculate the future Owner Earnings.

Find the present value of Owner Earnings by discounting with 30 yr T-bond rate.

Owner earnings = Net income + depreciation & amortization +/- one-time items – capital expenditures http://www.oldschoolvalue.com/blog/valu ... -flow-fcf/ “If we think through these questions, we can gain some insights about what may be called “owner earnings.” These represent (a) reported earnings plus (b) depreciation, depletion, amortization, and certain other non-cash charges such as Company N’s items (1) and (4) less ( c) the average annual amount of capitalized expenditures for plant and equipment, etc. that the business requires to fully maintain its long-term competitive position and its unit volume. (If the business requires additional working capital to maintain its competitive position and unit volume, the increment also should be included in ( c) . However, businesses following the LIFO inventory method usually do not require additional working capital if unit volume does not change.)” – 1986 Berkshire letter

ต้องเป็นบวก ไม่ใช่ หัก

slide 19

#8 – “Owner Earnings”

Net income + depreciation + depletion + amortization

- capital expenditure

additional working capital

Was it a) because the term never existed in 1986? b) or did he just forget about it?

I believe it is neither.

If you note the bolded section of Buffett’s owner earnings, he clearly states that changes in working capital should also be in (c). That is, if a company is required to increase working capital in order to maintain its position and operations, that’s really an increase of maintenance capex.

Assuming the company could continue to grow Free Cash Flow at 21.8% a year for ten years, and then slowed to 5% thereafter, and assuming Buffett wanted a 15% or more average annual return, you could value Coca-Cola at $22.3 billion, or $59.16 a share in 1988.

For new readers: The $22.3 billion is made up of $2.09 billion of Shareholder Equity and the net present value of the estimated $98.89 billion of future cash flow, discounted at 15% for a handsome return. Here is why we look at these numbers. See Calculating The Value Of A Business for a more detailed explanation of the calculation.

สรุปคือ มูลค่าคำนวณได้ $59.16ต่อหุ้น ณ 1988

2.

เห็น MOS 24% and 41%. โดย ราคาตลาด ตอนนั้น แค่ $35 and $45.25

The Purchase

At a 25% discount to value, Coca-Cola could have been purchased at any time at or below $44.37. In 1988, the company’s stock traded between $35 and $45.25, giving Buffett a discount between 24% and 41%.

source: http://www.barelkarsan.com/2008/11/warr ... art-3.html

The renewed core operating focus at Coca-Cola resulted in significant growth of net cash flow. The cash flow was put to use by initiating the first ever stock buyback program in 1984, increasing shareholder dividends and reinvesting in the business. Since 1984, the company has bought back 25% of their shares.

In 1988, the time when Buffett made his investment in Coca-Cola, the company had a price to earning ratio of 15 times and a price to book ratio of 5 times. On the surface, this didn't seem to be a value play, but as Buffett has said, the value of a company has nothing to do with price and everything to do with what the expected future discounted cash flows will be during the life of the business.

In 1988, Coca-Cola produced owner earnings of $828 million at a time when the long term U.S treasury rate yield was around 9%. Coca-Cola grew owner earnings at a annual rate of 17.8% between 1981 to 1988.

Using the Coca-Cola's 1988 owner earnings, the 9% treasury yield as a cash flow discount and a growth assumption for owner earnings of 10% for 10 years followed by 5% thereafter, results in a value for the company of $32.5 billion. At the time Buffett purchased Coca-Cola in 1988, the market cap of the company was just $14.8 billion.

Trailing 12 months figures can be calculated by subtracting the previous year's results from the same quarter as the most recent quarter reported and adding the difference to the latest fiscal year end results

โดย Beginning Value หมายถึง มูลค่าในปีเริ่มต้นก่อนการคำนวณ Ending Value หมายถึง มูลค่าในปีสุดท้ายของการคำนวณ No. of Years หมายถึง จำนวนปีที่ใช้ในการคำนวณ

source:http://as-th.listedcompany.com/glossary.html