Staples Is Well-Positioned To Capitalize On Eventual Industry Rebound

As the "best in breed" office supplies retailer, Staples (SPLS) is a fantastic business that provides the potential for long-term free cash flow expansion through its Retail (40% sales, 10.7% op margin), Delivery (40% sales, 9.5% op margin, and International (20% sales, 3.0% op margin) business segments. Despite low investor sentiment due to macro concerns, there are significant long-term tailwinds in place for the patient investor. Based on my analysis, the current market price of $15.00 is approximately 40% below the company’s true intrinsic value, providing an attractive entry point with a comfortable margin of safety.

The office supplies industry has taken a significant hit in recent years due to the global economic downturn, but SPLS has been able to weather the storm and is positioned well to capitalize on an eventual industry rebound. Unlike many of its competitors, SPLS has continued to invest in high-growth areas (Technology, Copy & Print) while steadily increasing retail store count in North America (+170 since 2007) and international markets (+77 since 2007). The 2008 acquisition of Corporate Express illustrated the company’s focus on the Delivery segment (serves F500 and other corporate customers), which eventually should feature margins 1-3% higher than Retail while requiring less capital. The majority of SPLS' profits are now generated online (second largest online retailed behind Amazon), which offers a more visible earnings stream because SPLS uses its own fleet of trucks and ~60% of these sales are under sizable long-term contracts with corporate clients. Once full synergies are achieved by 2014, SPLS' long-term targets are 12% Delivery operating margins (9.5% in 3Q11; 8.5% in 2010) and 9% consolidated margins (8.1% in 3Q11; 6.6% in 2010).

SPLS currently has an attractive balance sheet that features a high cash balance of $1.1BB and moderate LT debt of $1.6BB (down from $2.5BB at 2009 year-end). Despite the difficult economy, the company has continued to generate impressive free cash flow which it has used to delever as well as return to shareholders via dividends and share repurchases. I project $1.2BB in FCF in 2012, suggesting a FCF yield of 12%. In addition, ROIC of 11.8% is down from five years ago but trending upward; SPLS ROIC is generally in-line with WMT and well ahead of direct peers OMX (3.4%) and ODP (2.5%). Based on my analysis, I project SPLS could increase ROIC to 14-15% in two years. Another key differentiator for SPLS is its strong, stable management team that has largely been kept intact over the last 15 years. Current CEO Ron Sargent has been with the company since 1989 and CFO John Mahoney has been on board since 1996; in comparison, ODP CEO Neil Austrian came on board in 2011 (after Steve Odland’s disappointing six-year tenure) and OMX CEO Ravi Saligram joined in 2010. Neither Austrian nor Saligram have office supplies industry experience. SPLS management has been through ups and downs in the office supplies space and is much better prepared to understand and react to unique industry pressures.

Near-term Street expectations for SPLS are low, but I believe the company is a very attractive investment for the patient investor with a 3-5 year horizon. If the global recession continues to linger through 2012, SPLS is in the best position of all office supplies retailers to manage through it due to its strong balance sheet and ability to generate sizable free cash flow (+$1BB the last four years). Management will continue to invest in high-growth areas, increase dividends, and repurchase shares (“Probably the best investment that we could make as a company would be to buy back our own shares at this level, because we think the stock is on sale.” – CEO Ron Sargent at 09/2011 Goldman Sachs conference). However, if the global economy shows meaningful improvement, SPLS will gain market share and increase profitability due to its strong competitive position in North America and international markets, dominant presence in Delivery and online sales, and untapped operating synergies associated with the Corporate Express acquisition. In summary, SPLS’ strong balance sheet, ability to generate significant free cash flow, upward-trending ROIC, and shareholder-friendly management makes the company an incredibly attractive investment.

Potential Catalysts

Initial 2012 Guidance: Despite solid results from the NA Retail and NA Delivery segments in 3Q11, consensus estimates remain low for 2012 after SPLS lowered expectations throughout 2011. Initial 2012 guidance is expected with 4Q11 results, and collectively the Street is expecting 2012 EPS of $1.47, implying YOY growth of approximately 8.8%. However, if management continues to focus on repurchasing shares at low market prices, I project approximately $0.04 in EPS accretion with another ~$600MM in repurchases in 2012. If SPLS is also able to show meaningful operational improvement, I believe 2012 consensus estimates will prove conservative.

Operational Improvement in International Segment: Investors and analysts appear to be holding off on SPLS until the company can show meaningful improvement in the International segment. Disappointing International results have dominated the Q&A session of recent earnings calls, while analysts generally ignored the excellent free cash flow, shareholder-friendly increases in repurchases and dividends, and market share gains in NA Delivery.

Additional Share Repurchases (or Insider Buying): SPLS initiated a stock repurchase plan in 2010 after lowering its debt level from the Corporate Express acquisition. Management is targeting $600MM in share repurchases in 2011, and it appears reasonable to assume a similar level in 2012 due to the large amount of cash the company generates. Insider buying would also be a positive signal.

Bull Case

"Best in Breed" Office Supplies Retailer with Strong Infrastructure in Place. Instead of halting investment over the past few years due to the economy, SPLS has grown NA stores, increased international presence, and drastically improved their reach in the Delivery segment with CXP acquisition. SPLS is in the best position of all office supplies retailers to expand margins and FCF over the next 5 years.

Significant International Reach with Improving Profitability. Management is targeting 7.5% operating margins in Europe within three years and eventually a similar margin for the total intl business (3.0% in 3Q11) by focusing on G&A adjustments (150-200 bps) and supply chain improvements. SPLS has 377 total international stores, including 200+ in Europe and 20+ in China.

Impressive Valuation/Cash Flow. SPLS generates $1BB in FCF per year, and has steadily repurchased shares and paid down debt despite core business difficulties. ROIC of 11.8% is well ahead of direct industry peers and has further upside. FCF yield is 10% with potential for 12-13% in 18-24 months.

Strong Management Team; New Intl Hires. CEO Ron Sargent has been with SPLS for 23 years, much longer than CEO counterparts at OMX and ODP, and has been through up and down cycles before. SPLS reshuffled Intl leadership in late 2010 to address disappointing performance.

Improving Margins via CXP Synergies. Management is targeting 9% operating margins by 2014 (6.2% in 2009) and 12% op margins in delivery once full synergies are achieved and CXP integration is completed.

Industry Consolidation. There is concern that the office supplies industry has too many competitors, and greater industry consolidation could provide more breathing room for all market participants.

Bear Case

Potential Acquisition of OfficeMax (OMX) or Office Depot (ODP). Both companies have jeopardized their competitive positions over the last two years by decreasing capex below maintenance levels, closing stores, and selling real estate. An acquisition by a better capitalized firm could potentially challenge SPLS' industry position.

Inability to Increase International Profitability. Outside of Germany, SPLS has struggled recently in Europe and Australia recently due to macro issues. However, SPLS is profitable in every European country outside of Belgium, and high-growth markets Brazil, India, and China have generated solid overall growth and reduced operating losses in-line with internal plans.

Extended Pressure on U.S. and European Employment. SPLS core business is very much tied to labor, and the company may struggle to generate meaningful growth until unemployment rates improve in its mature U.S. and European markets.

Greater Competition from Online or Big Box Retailers. While SPLS has performed much better than direct peers OMX and ODP, the company will continue to face greater competition from Wal-Mart (WMT) and Target (TGT) in the retail setting and Amazon (AMZN) in the online setting.

In investing, there are few things more satisfying than finding a stock hiding in plain sight.

When a company's story is generally misunderstood, savvy investors are often given a chance to pounce at a great price.

I think the market is currently underestimating the No. 2 Internet retailer in America. Here's how under the radar it is: If I gave you three guesses, I bet you couldn't name it.

Amazon.com (Nasdaq: AMZN ) is No. 1. But the No. 2 online retailer is Staples (Nasdaq: SPLS ) . Yes, it has more online sales than Wal-Mart (NYSE: WMT ) , Dell, or Apple.

Surprised? I was. And the surprises kept coming the further I dug.

If you asked the average Joe for his view on Staples, he'd mention its physical stores and maybe the "easy button" from the ads. But Staples isn't Best Buy or RadioShack. Unlike regular bricks-and-mortar retailers, it gets roughly half its business from delivery operations, which are predominantly done online. And its sales are 80% from business customers.

Accentuating these facts, Staples has two competitive advantages:

1.Its size, buying power, and private label strategy combine to create a low-cost provider in the office supplies market, making it hard for direct competitors Office Depot (NYSE: ODP ) and Office Max (NYSE: OMX ) to survive, much less compete.

2.Its business focus allows Staples to differentiate from low-cost threats including Amazon.com, Wal-Mart, and Costco.Its established relationships and hand-holding strategy combine to make life easier on purchasing managers at medium-sized businesses, Staples' sweet spot. If you doubt how big a factor ease of use plays versus cost in corporate America, just think about how much companies pay for last-minute business flights versus what its employees will pay for vacation flights.

At this point, you may be convinced Staples is more than meets the eye, but you're probably wondering where the growth comes from. After all, office supplies don't come to mind when you think "growth industry." Staples already has a significant international presence (one-fifth of sales), but much of that is in Europe, which is struggling with its sovereign debt and resulting economic issues now. There's some growth in physical storefronts each year, but it's a very small percentage.

No, Staples' opportunities for growth are also a bit hidden. Remember we talked about how Staples seeks good relationships with purchasing managers at companies? Like McDonald's getting you to buy some fries with that Big Mac, Staples is looking to expand the average spending by its customers by upselling -- in this case, to print and copy services, facilities and break room supplies, and technology products and support. Basically, it's trying to be a user-friendly, one-stop shop in the business-to-business market.

In addition to broadening its products and services, Staples is looking to expand its margins by selling a greater percentage of its private label supplies. In other words, its store brand products. Assuming similar quality, it's a win-win for Staples and the customer. Customers save 10%-15% versus brand name supplies and Staples generates higher margins. Staples has already been a master at this -- generating a quarter of sales from private label items. It's looking to push that higher.

And Staples (as well as Amazon.com, Wal-Mart, and Costco) has an opportunity to pick apart weaker competitors -- specifically Office Depot and Office Max. While Staples has shown growth and consistent profitability over the last few years, we see declining sales and profitability struggles for the other two. Their pain can be Staples' gain.

So I hope it's clear by now that Staples is much more than the red storefronts you drive by -- it's a smartly managed business-to-business powerhouse. And it's selling near five-year lows, at less than 10 times next year's expected earnings.

Let me be blunt, in the office supply superstore arena, the battle has already been won. These companies have been battling it out with each other for years. They also have been trying to fend off competition from more traditional retailers like Walmart and Target. If you believe there is a future for focused superstores, there is one company to consider adding to your buy list: Staples (NASDAQ: SPLS). Unfortunately, the two companies that compete with Staples might both be good candidates to short. These two underdogs are OfficeMax (NYSE: OMX) and OfficeDepot (NYSE: ODP).

Just looking at the companies side by side speaks volumes. Take a look at their expected growth and valuation and you may see what I mean.

Name

Price

P/E on '12 earnings

Growth expected

PEG

Yield

Staples

$15.47

10.38

9.86%

1.05

2.58%

OfficeMax

$5.86

9.93

-0.68%

-14.6

0.00%

OfficeDepot

$3.08

38.5

30.30%

1.27

0.00%

At first glance Staples looks like the best value. It is the only company of the three that pays a dividend. It also has the lowest PEG ratio. Some might say, but what about OfficeDepot's expected growth? Shouldn't I consider buying their stock, if they have the highest expected growth rate? The answer is no. I don't believe analysts know what to expect from OfficeDepot. If you look at what the three companies have done compared to analysts estimates, you can see a pattern there too.

Analysts seem to know what Staples is going to do, they are less sure about OfficeMax and they are generally not close on OfficeDepot. This is what gives me confidence that Staples expected growth of 9.86% is likely to occur. Where OfficeMax is concerned, they have a negative expected growth rate. Even if they beat earnings by the amount they have been, that's not going to make OfficeMax a buy. Where OfficeDepot is concerned, the projected growth rate of 30%+ seems like a lot of smoke and mirrors. With the company missing estimates twice in the last year by 100% I don't believe analysts really know what OfficeDepot will do.

As another point of comparison, of these three companies, only Staples has repurchased shares in each of the last 4 quarters. While OfficeMax has made share repurchases in 3 of the last 4 quarters, their cash flow argues that this will not continue. OfficeDepot is going the opposite direction and has issued more stock than they repurchased in the last year. Staples clearly leads the way when it comes to managing their share count. This bodes well for future earnings per share and could lead to some nice surprises down the road.

The most telling factor I see to differentiate between these three companies, is their cash flow and balance sheets. Staples leads the way by a large margin in both categories. Staples has produced about $0.08 of free cash flow per $1 of assets in the last year. In addition, they have the strongest balance sheet with a debt-to-equity ratio of 0.219. By comparison, neither OfficeMax or OfficeDepot have positive cash flow in the last year. In fact, OfficeMax shows negative cash flow of $0.018 per $1 of assets, and OfficeDepot shows negative cash flow of $0.023 per $1 of assets. When it comes to their balance sheets, OfficeMax and OfficeDepot can't compete with Staples. Each company has a higher debt-to-equity ratio than Staples, with OfficeMax at 0.351 and OfficeDepot coming in at 0.868.

So you have a choice, a company that is cash flow positive, pays a dividend, is growing, and has the best balance sheet. Or you can buy one of its two competitors. Both cash flow negative and have worse balance sheets. I'm willing to back up my assumptions by making CAPSCalls on all 3. Staples get the green thumbs-up, the other two get the red thumbs-down. Like Staples says, “that was easy”.

ไม่น่าเชื่อว่าหลังจาก Best Buy สามารถทำให้คู่แข่งอันดับสอง Circuit City ล้มละลายได้ การขยาย retail stores จะทำให้ Best Buy กลายเป็น Electronic Retail Store เบอร์ 1 โดยลืมคิดการขยาย online sale (หรือคิดแล้วแต่สู้ Amazon กับ Staples ไม่ได้?)

ต้องมาเจอกับจุดตกต่ำ Stand Alone electronic retails

Best Buy CEO Resigns: Is the Company Going Under?

Best Buy (BBY) CEO Brian Dunn resigned today. While Wall Street's immediate reaction was to drive the electronic retailer's shares higher on the resignation (read: firing), the news is unlikely to delay the company's descent into irrelevance and/or bankruptcy.

Dunn has overseen more than his share of missteps since becoming CEO in mid-2009. Of these failings the most notable was the company's inability to deliver goods purchased online during Black Friday 2011, and not inform customers until several days before Christmas. Adding insult to injury, Best Buy offered little more than a meek "sorry" and excuses to those left with nothing under the tree.

The Christmas nightmare destroyed Best Buy's e-commerce ambitions and, with it, the company's last best chance at survival.

Despite a less-than-stellar time running the company, Dunn was more a victim of changing times than his own ineptitude. The enormous stores Best Buy used to put one-time competitor Circuit City out of business are an albatross around the company's neck, but it isn't just the stores sucking the life out of the chain either.

Best Buy is dying because the free standing consumer electronics stores model is obsolete. The albums and CDs that once occupied the most valuable space in gigantic Best Buy stores are not longer selling. Console video games are losing share to tablets. High definition wall-mounted televisions are commodities readily available at Wal-Mart (WMT), Target (TGT), or online.

A web search yields far more information about any electronics product than any sales associate ever could and nobody needs help wiring their stereos anymore.

Best Buy has been trying to compensate by going into office supplies, appliances and furniture. Competing with Staples (SPLS), Sears (SHLD), and Ikea isn't a solution; it's desperation.

The snarky suggestion that customers "shop at Best Buy then go home and buy at Amazon.com (AMZN)" is wrong. No one goes to Best Buy at all. The stores have nothing to offer that you can't get more easily and cheaper elsewhere.

Brian Dunn's departure wasn't a sign of life but a death rattle. Wall Street knows this, which is why the stock's pop quickly turned into a decline. Best Buy sacked Dunn because it was cheaper than jumping straight into Chapter 11.

Ultimately Dunn will be better off for having left now rather than having gone down with the Best Buy ship.

At Staples, we take great pride in our consistent execution and our

ability to evolve and meet the changing needs of our customers.

Throughout our 25 year history we’ve succeeded by setting

aggressive goals, acquiring and retaining customers, and being

accountable for our performance. We took the same approach

in 2011 and made progress on many of our key initiatives, despite

the challenging economic environment.

In 2011, we grew sales to $25 billion, drove eight percent earnings

growth, and generated $1.2 billion in free cash flow. We returned

nearly $900 million to shareholders through dividends and share

repurchases, and we invested just under $400 million in capita expenditures to further differentiate our offering. While our industry leading financial results were solid, we continue to work hard and press our advantage to position the company for long term growth.

In North American Delivery, we did a good job with customer acquisition and retention and were once again recognized for our industry leading customer service. We made big investments to improve the functionality, performance and usability of Staples.com. These have helped to provide a better customer experience and build top-line momentum in this business. Over the past few years, we’ve invested in

marketing, pricing, associate training, and an expanded assortment in adjacent categories like facilities and breakroom supplies. These are starting to pay off. During 2011, we achieved double-digit sales growth in the facilities and breakroom category and ended the year with an $800 million business in North American Delivery. We’re in the fina innings of the Corporate Express integration. During 2011, we completed our warehouse systems integration in North America and began the process of transitioning all of our Contract customers over to our new and improved ordering platform, StaplesAdvantage.com.

In North American Retail, we pulled back on new store openings and increased our focus on improving the productivity of our existing stores. We continued to make investments to become a leader in copy and print, business technology and technology services. In copy and print, we broadened our assortment and improved the quality of our offering. We also expanded our copy and print sales force to build on our low single-digit market share in this category. Over the past two years we’ve remodeled the technology area in more than half of our stores to improve how we sell and service technology products. This helped to drive strong sales growth in categories like tablets and e readers, as wel as our EasyTech business during 2011. We also made a big push into the mobile phone business to address an essential need of small business customers, and we now have a mobile department in 500 stores across the United States.

In International Operations, we had a difficult year on both the top and bottom-line, and we did not make progress against our profit improvement plans. While the Internationa team did a good job controlling expenses, sales trends were much weaker than we anticipated. We were impacted by weak performance in both our European Retai and Australian businesses, as well as headwinds from the European debt crisis. Despite the difficult trends, we continued to drive solid top-line performance in the European Contract business. Over the past two years, we’ve had great success with the launch of our mid-market Contract offering in the United Kingdom, and during 2011 we introduced this concept in Germany.We also continued to reduce losses in emerging markets like China, and remain on a path to profitability. We expect the demand environment in Internationa Operations to remain soft throughout 2012. We’ll continue to carefully manage expenses and focus on re-establishing our value proposition with small business customers, as we work hard to gain share in these highly fragmented markets.

Staples (SPLS) dominates the office supply store space: there is no reason to think it won't one day push its principle competitors to the curb. But the shares languish despite the strength of the business and healthy (and steady) cash flow. A speculator might not be able to get a "pop" out of this one, but patient investors take note: Staples might hold its dominate position in the future--a long profitable future. The share price does not reflect the safety of the returns (which would find its mathematical expression in a lower discount rate used). This "pick" is as much about safety of principle as much as it is about the adequacy of return.

North American Retail

We are all familiar with the "easy button" ads and with their retail outlets, but that represents less than half of Staples' operating income. In 2011, consumer facing retail made up 38% of Staples revenue, 45% if its operating income and a similar amount of its capital expenditures. It is making moves into electronics retailing by moving products to the front of store (among other design changes) and reemphasizing electronics generally. For instance, in the May Q1 2012 conference call, CEO Ron Sargent said:

During the first quarter, sales of mobile phones and accessories nearly doubled, and we achieved strong double-digit top line growth in new technology products like tablets and eReaders.

This corroborates with plans stated in Sargent's letter to shareholders written in April 2012:

Over the past two years we've remodeled the technology area in more than half off our stores to improve how we sell and service technology products. This helped to drive strong sales growth in categories like tablets and e-readers, as well as our EasyTech business during 2011. We also made a big push into the mobile phone business to address an essential need off small business customers, and we now have a mobile department in 500 stores across the United States.

Staples makes a little less than half of its money from retail where it dominates the competition. In North America, for example, Office Max (OMX) has 978 stores with average revenue per store of $3.5 million, Office Depot (ODP) has 1,131 stores with average revenue of $4.3 million per store, and Staples has 1,900 stores with an average of $5.08 million per store--or it has about 67% more stores, which make 18% more on average compared with their nearest competitor. Even while its retail is a success (historically speaking), the majority of its revenue and income is from its North American Delivery segment.

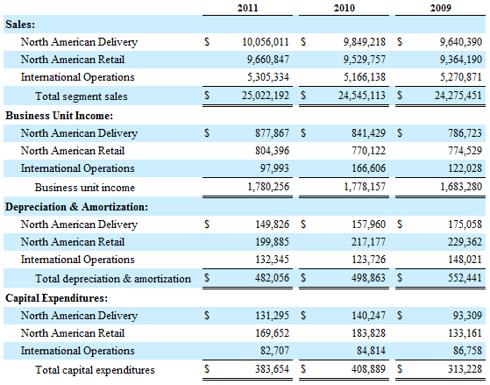

First, some segment Information (Staples 2011 10-K, page C-33; in thousands):

Notice above the low "business unit income" from "international operations" compared with its proportion of revenue. Management is looking to turn around the overseas segment and have reduced headcount by about 300 positions in an effort to improve profitability. We will see that Staples can still be considered undervalued even while ignoring future growth outside North America.

North American Delivery

The majority of North American Delivery customers place their orders online, making Staples the 2nd-largest online retailer in the world, after Amazon (AMZN) (See Staples 2011 10-K, page 1; for further evidence, see rankings here). Given the overall depressive effect the success of Amazon is having on brick-and-mortar retail, if such an effect is present in the shares of Staples--it is unjustified.

Of Staples revenue, 27% was from proprietary brands which both (i) sell for cheaper than national brands and (ii) provide a higher gross margin. Staples would like to push that figure up to 30% (2011 10-K, p. 3).

Part of Staples' plan to continue to grow is to move out from core office supply categories, into "adjacent" categories, such as "facilities and breakroom supplies." As of Q1 2012, these new categories had increased by 20% year over year. To further expand from core categories, Ron Sargent noted that Staples is "building on our success in facilities and breakroom supplies with an expanded assortment of safety and industrial supplies" (Q1 2012 Conference Call Transcript).

The Downside Is Limited

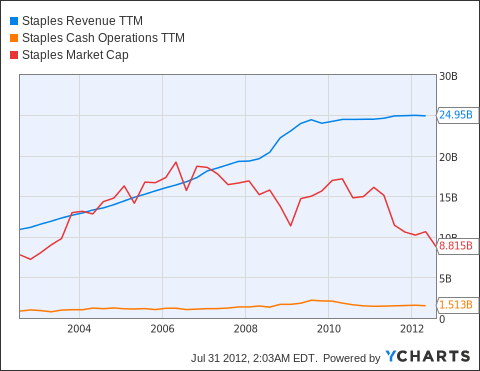

Since January 2011, Staples has decreased its debt by 22%. Throughout the same period, shares outstanding have decreased 4.3%. One can see from the chart above that while revenue growth has slowed, Staples' market capitalization has fallen precipitously. Further, Staples is registering its lowest price-to-sales ratio ever.

Staples' primary business is delivering necessary office supplies to businesses. Business purchases tend to be more consistent and less fickle than consumer purchases. They build long-term relationships and large contract customers come to rely on their supplier, i.e., Staples. Staples' business customers are unlikely to give up shopping at Staples in the near future. Further, competitors hold weak and falling market positions. It could turn out that the office supply space is like the electronics retail space and we will see Staples' principle competitors fade away like Circuit City.

Valuation

With 2011 free-cash-flow at around $1,050 million (and growing moderately), the price to free-cash-flow ratio is:

Market Capitalization / Free-Cash-Flow = P/FCF

$8,780 million / $1,050 million = 8.36

On a trailing twelve month basis, it has a higher free-cash-flow yield than 85% of the S&P 500 (and some of those 15% are financial companies which shouldn't count since the free-cash-flow concept doesn't apply in the same way to them). With a FCF yield of almost 12%, possible long-term growth prospects and a dominate market position, Staples looks like a good long-term retail holding.

Another author on this site mentioned that Staples needs a "catalyst" for growth. While I think revenue growth will be probably not be much above GDP in the near term, there is also no near-term catalyst, which might result in a change of opinion about the shares. While the shares present a good long-term holding, they may continue to languish while people ignore the strength of the business. There is no "phase-change" or transition-catalyst in sight to call investors to rethink their valuations of Staples. Therefore, for those looking for quick capital appreciation, Staples might not be the stock for you. But downside is limited, and the return of the shares (overtime and barring any unforeseen cataclysm) will very likely exceed the returns offered by other companies.

Boring companies don't get much love, but boring companies frequently offer safe and satisfactory long-term returns.